This article was originally published by Law360 on November 6, 2020.

Globally, companies continue to face the economic realities created by the COVID-19 pandemic. As organizations initiate settlement talks with regulators, they might consider raising an inability-to-pay claim to reduce significant fines.

Successful inability-to-pay claims have been on the rise over the past few years, particularly after the U.S. Department of Justice's Criminal Division issued a memorandum in 2019 providing guidance for prosecutors to follow when corporations raise inability-to-pay claims.

These claims may also increase in DOJ Civil Division enforcement actions, as the Civil Division issued its own inability-to-pay guidance in September, which largely mirrors the Criminal Division's guidance.1

Impact of 2019 Guidance on Inability-to-Pay Claims

Historically, prosecutors could consider a company's financial situation when assessing fines or penalties. In the years leading up to the release of the 2019 guidance, corporate defendants received fine and penalty reductions due to their inability to pay the full amounts proposed under the U.S. sentencing guidelines.

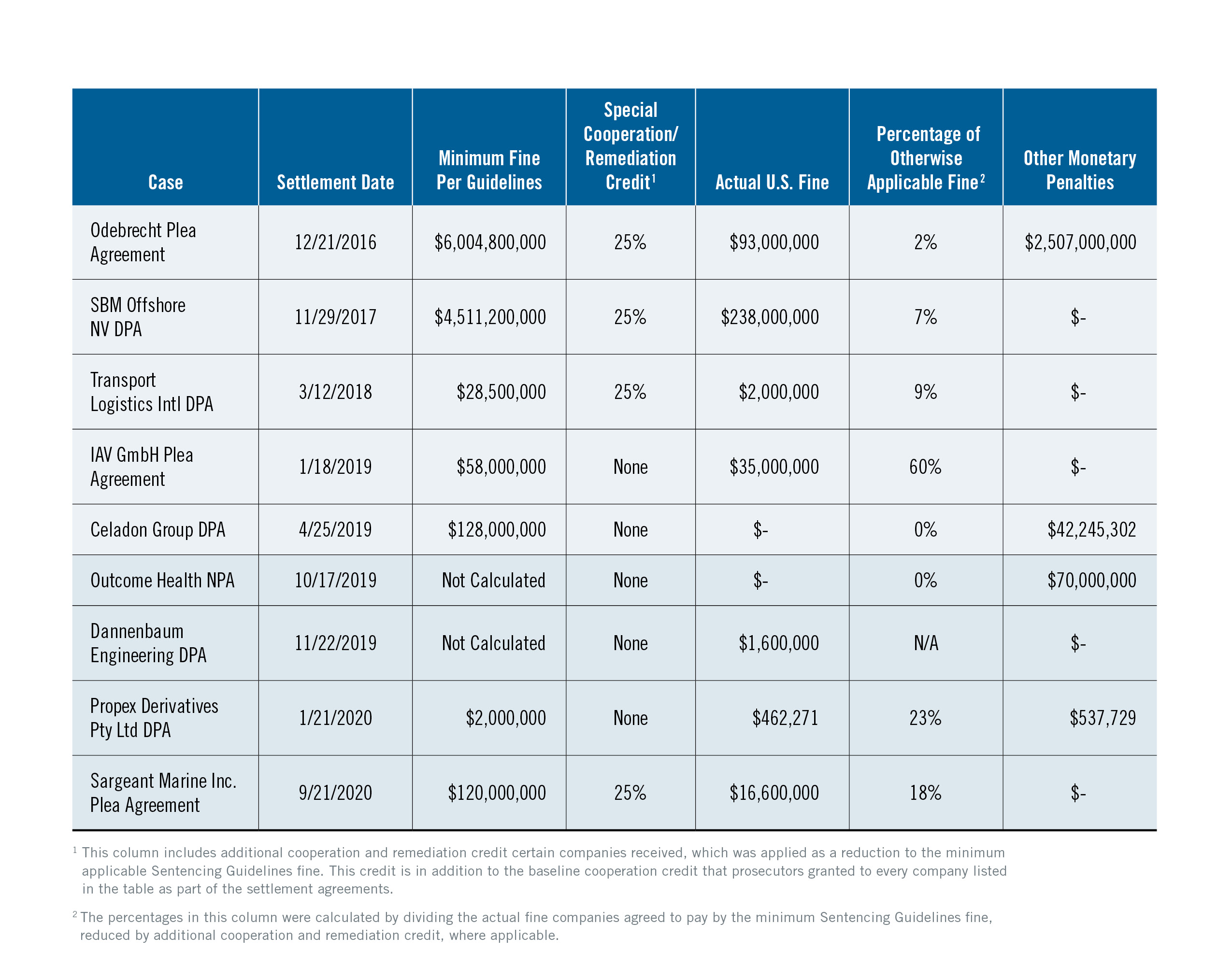

The 2019 guidance did not introduce a new practice but instead provided transparency and a framework for a practice already in existence. Following the 2019 guidance, the number of settlements citing inability to pay as a consideration in reducing penalties significantly increased. The following table outlines a number of settlements that considered companies' inability to pay fines both before and after the DOJ issued the 2019 guidance.

While the settlement agreements do not include a detailed financial analysis supporting the inability-to-pay reductions, multiple agreements note that fines were reduced to "avoid substantially jeopardizing the continued viability" of the defendant corporation.2

The DOJ appears to value preserving the defendant corporation's continued existence and prioritizing victim restitution payments. For example, Celadon Group Inc. and Outcome Health were only required to pay victim restitution payments and were not required to pay additional fines.

The DOJ also appears to take into account fines paid to foreign regulators when assessing inability-to-pay claims. For example, Odebrecht SA paid a fine to U.S. regulators that was well below the minimum sentencing guidelines, but also paid over $2.5 billion in fines to Brazilian and Swiss regulators. Similarly, U.S. prosecutors considered penalties SBM Offshore NV had already paid to Dutch authorities and likely penalties the company would pay to Brazilian authorities when determining a fine reduction.

While settlements have generally decreased in 2020, Sargeant Marine Inc. successfully raised an inability-to-pay claim in a September settlement, resulting in a greatly reduced fine.

Establishing an Inability-to-Pay Claim

Organizations in settlement negotiations that are struggling financially might be able to successfully raise inability-to-pay claims. The organization then bears the burden of establishing this claim.3

Prosecutors will consider a range of factors, including collateral consequences such as (1) the penalty's potential impact on an organization's ability to fund pension obligations or provide the amount of capital, maintenance or equipment required by law or regulation; and (2) whether the penalty is likely to cause layoffs, lead to product shortages, or significantly disrupt competition in a market.

The fine or penalty should only be reduced to the extent necessary to avoid (1) threatening the continued viability of the corporation, (2) causing especially severe adverse collateral consequence, even when they do not necessarily threaten the corporation's viability, or (3) impairing the organization's ability to make restitution to victims.4

As demonstrated by the reduced penalties in recent settlements, ranging from 0% to 60% of the minimum fine suggested by the sentencing guidelines, prosecutors exercise tremendous leeway once an entity has established a satisfactory inability-to-pay claim.

Agencies seem to rely heavily on independent analyses to verify an organization's financial situation, especially in cases in which the sentencing guidelines recommend a relatively high-fine range. If a company can substantiate claims that paying the recommended fine would jeopardize its continued viability and lead to layoffs or a significant disruption of competition in the market, leniency is more likely.

For this reason, businesses and their counsel may consider working with outside experts to put forth reasonable positions after an independent evaluation of company financial statements.

Third-party experts can help gather and present objective data on how various penalty scenarios will impact the business. This may include seeking to establish that separate discussions among various federal, industry and local regulatory parties that may have an interest in an enforcement action are not only inefficient for regulators' time and resources but may also "substantially jeopardize[e] the continued viability of the Company."5

Other common areas of scrutiny and challenge include:

- Correlation of company insolvency to the suggested penalty;

- Ordinary course of business forecasts prepared before the suggested penalty;

- Trending historical results and achievement of prior budgets; and

- Market, industry and economic conditions that may impact the company's financial situation.

Further, good faith efforts by the organization to remediate its underlying compliance program and enhance its internal control framework are generally viewed positively by regulators. As seen in several of the above settlements, up to a 25% reduction in penalties has been given as additional credit for cooperation and remediation.

Key Takeaways

For companies that hope to establish an inability-to-pay claim, documentation is key. Particularly for organizations involved in investigations, independent auditors regard contemporaneous documentation as more persuasive than information created once settlement talks begin.

If records were not proactively maintained preinquiry, forensic technologists or data analysts can be helpful in organizing disparate or complex business information to support an inability-to-pay claim.

As more organizations are affected by the COVID-19-related economic downturn, criteria for successfully reaching a reduced settlement are likely to become more stringent. With the right documentation and support, companies can best ensure their continued viability when faced with potentially large fines.

- https://www.justice.gov/civil/page/file/1313361/download.

- https://www.ussc.gov/guidelines/2018-guidelines-manual/2018-chapter-8 § 8C3.3.

- https://www.justice.gov/opa/speech/file/1207576/download.

- https://www.justice.gov/opa/speech/file/1207576/download at 4.

- https://www.ussc.gov/guidelines/2018-guidelines-manual/2018-chapter-8 § 8C3.3.

Stay Up To Date with Ropes & Gray

Ropes & Gray attorneys provide timely analysis on legal developments, court decisions and changes in legislation and regulations.

Stay in the loop with all things Ropes & Gray, and find out more about our people, culture, initiatives and everything that’s happening.

We regularly notify our clients and contacts of significant legal developments, news, webinars and teleconferences that affect their industries.