Alternative asset classes continue to mature, grow and attract investors. From continuation funds to asset management consolidation, the industry is poised for a dynamic 2025.

The Asset Management industry is poised for a dynamic 2025 as visibility returns to stock markets, interest rate-afflicted asset classes emerge from dormancy, and nascent private market strategies demonstrate viability across economic cycles.

Optimism in Alternatives

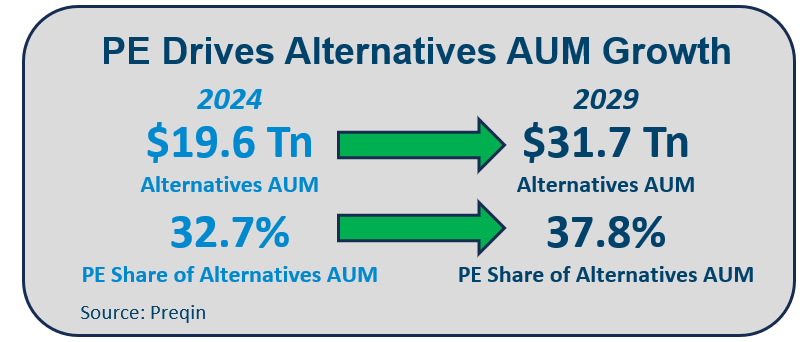

Global AUM across alternative asset classes is expected to expand at a 10% CAGR from 2024-2029 with Private Equity comprising a growing share, offsetting sluggish AUM growth in the Hedge Fund class, according to Preqin. Steady growth is projected for nascent strategies that thrived during the recent economic downturn including Private Credit, Infrastructure, and Secondaries with these asset classes expected to retain their utility in the foreseeable future.

Resurgence of Private Equity

Following two challenging years, the beginning of a monetary-loosening cycle and a more favorable exit environment are welcome news for private equity. Improving valuations are expected to encourage IPOs and M&A exits, mitigating the distribution pitfall and providing LPs the bandwidth to invest in new funds for GPs to deploy. Notably, Blackstone expects exit volumes in its North America PE business to double in 2025 (Reuters). While PE activity is unlikely to reach its 2021 heights due to valuation gaps and relatively high interest rates, industry experts expect an increase from 2024.

Long Term Demand for Continuation Funds

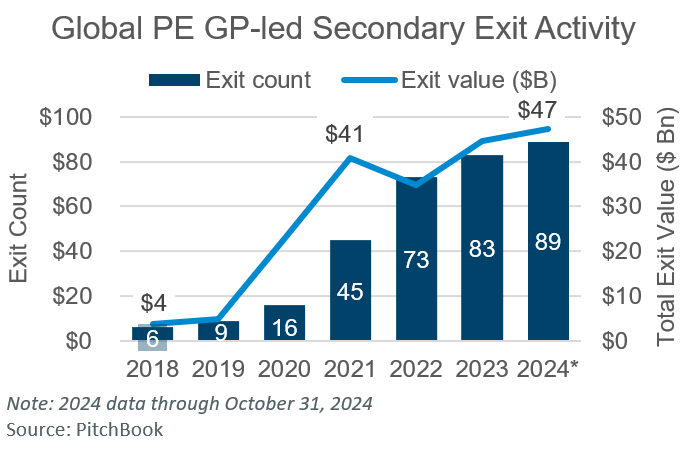

Despite an improving exit environment, the large backlog of mature PE-backed companies awaiting exits ($3.2 Tn of unsold assets through 2023, according to Bain & Co.) necessitates offramps to generate liquidity, providing optimism for secondaries markets. GP-led secondaries experienced a record 2024 with $47 Bn in GP-led secondary exits through October 31, 2024 (PitchBook), and momentum is unlikely to slow down in 2025.

Consolidation in Asset Management

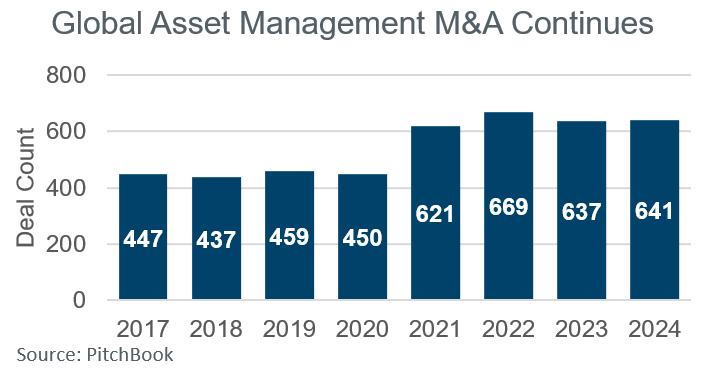

Since the pandemic, asset managers have increasingly acquired competitors to grow and diversify platforms, consolidate synergistic assets, and execute succession plans. In addition, traditional asset managers have acquired alternative managers to increase exposure to growing asset classes. Consolidation is expected to continue in 2025.

Intensifying Activism on ESG Issues

While the popularity of environment, social and governance (ESG) investing has diminished over the last couple of years, in many jurisdictions ESG compliance requirements have increased for investment funds that take ESG factors into account. Investor expectations and regulation have required large private capital firms to invest in ESG programs, including tracking and reporting on various manager and portfolio company metrics, relating to climate and workforce matters among other topics. In a finance survey, 89% of participating asset managers said ESG costs have risen materially over the past three years.

Investor expectations and regulatory requirements continue to evolve, including at the U.S. federal and state level and in the EU and U.K. 2025 is expected to be another year of significant change.

Stay Up To Date with Ropes & Gray

Ropes & Gray attorneys provide timely analysis on legal developments, court decisions and changes in legislation and regulations.

Stay in the loop with all things Ropes & Gray, and find out more about our people, culture, initiatives and everything that’s happening.

We regularly notify our clients and contacts of significant legal developments, news, webinars and teleconferences that affect their industries.