Necessity, they say, is the mother of invention, and the private markets industry has certainly responded to a period of intense fundraising turbulence with creativity and ingenuity.

Capital raised for traditional co-mingled funds fell nearly 24 percent last year, the third consecutive decline. The number of funds closed, meanwhile, fell to the lowest point since 2014 (click here for more information).

Even as exit activity appeared to resume, distributions as a portion of net asset value sank to the lowest rate in a decade. Still, private markets firms have found new ways to grow assets under management (AUM), even in a challenging market.

Access to Private Wealth Capital

Many best-of-breed managers continued to have success on the fundraising trail. European buyouts remained robust, with three funds closing on over $20 billion each (click here for more information). The trend towards manager consolidation among LPs remains strong.

GPs have continued to push deeper into new pools of capital, most notably establishing in-house or third-party feeder funds for high-net-worth investors. Some of the biggest private markets platforms have launched dedicated private wealth platforms, built around open-ended fund products.

The prevalence of these open-ended products has been particularly notable in the credit space, with the use of SICAV-RAIFs, allowing permanent exposure to assets held by the vehicle, together with a degree of liquidity well suited to private investors.

The so-called democratisation trend has been supported by regulatory changes. The European Long Term Investment Fund (ELTIF) 2.0 framework, which came into effect last year, is proving popular after replacing the previous structure which was seen as overly cumbersome and restrictive. In fact, 80 ELTIFs have been authorised over the past two years, compared to 79 between 2015, when the 1.0 version was launched, and 2022 (click here for more information). UCI Part II vehicles in Luxembourg are being used regularly by managers to access retail capital as well.

The UK equivalent of the ELTIF, meanwhile, the Long-Term Assets Fund (LTAF), is also gathering momentum. These open-ended vehicles are designed for both institutional and retail investors, critically expanding the viable pathway for UK defined contribution pension schemes to access private markets.

Looking ahead, the growing use of technology, including AI, is likely to further facilitate private wealth access to private markets. Managers are already experimenting with the automation of sub docs and side letters, for example, although the integration of AI into the fundraising process is still in the early stages.

SMAs Surge

Alongside ramping up private wealth fundraising channels, Separately Managed Accounts (SMAs) have been proliferating. The institutional fundraising market may have been dampened over the past few years, but appetite amongst some of the world’s largest investors, including sovereign wealth funds, remains robust.

These SMAs are often tailored to strategies that don’t fully align with the flagship vehicle. For example, they may be focused on a particular sub-sector, strategy or geography. SMAs may also be structured for full platform exposure, encompassing a commitment to multiple different funds across jurisdictions or asset classes.

SMAs have historically tended to involve closed-ended funds but a growing number are now structured as open-ended products, with distributions from the underlying funds immediately being recycled into new opportunities, supporting capital accumulation for investors not seeking short-term distributions.

Internationalise Your LP Base

Another strategy for growing AUM involves managers expanding the geographical scope of their LP base. Of note is the increasing number of US managers directly deploying Luxembourg limited partnerships or SCSps, without engagement of a European AIFM, to access international investors.

Following the introduction of the Alternative Investment Fund Managers Directive (AIFMD), the initial assumption was that in order to access European capital, an alternative investment fund managed by a European manager would be necessary. Many US-based firms therefore raised Luxembourg funds and set up Luxembourg managers, with the requisite teams on the ground to satisfy tax substance rules. Others hired third-party authorised administrators to fulfil the AIFMD requirements.

Now, many European investors are not demanding a fully AIFMD-compliant structure. These investors will typically not accept an offshore fund, but they do not require full AIFM status. Managers are therefore increasingly setting up Luxembourg SCSps, which are then managed out of their existing US SEC registered investment advisers or UK managers, for example.

These funds cannot access the full European marketing passport, but they can be privately placed in chosen jurisdictions. This simplified and less costly approach is proving highly effective.

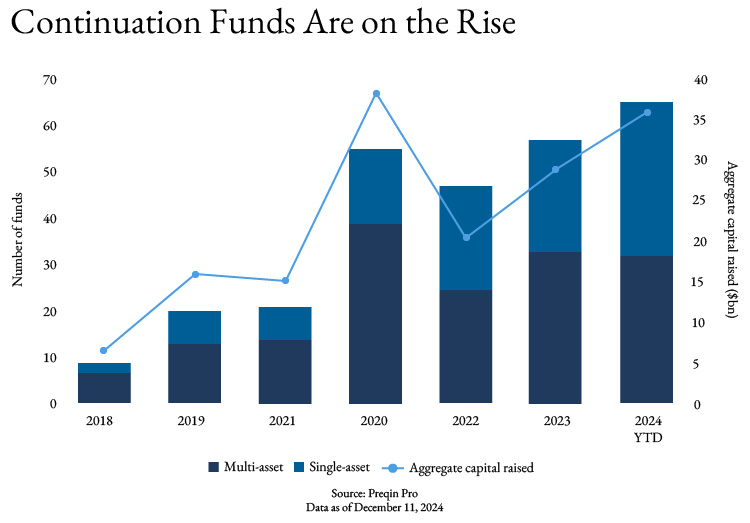

Continuation vehicles and co-investments

Continuation vehicles have played a key role in maintaining private markets momentum. Not only have these vehicles allowed managers to hold onto their most promising assets, whilst releasing much needed distributions to LPs, they have also provided managers with access to the vast pool of capital that is the secondaries industry.

As continuation vehicles have become increasingly common, a best practice playbook has emerged around conflict resolution and alignment, including exploration of super carry structures, helping the market opportunity grow further.

Co-investment also remains an important tool in a stilted fundraising environment, particularly in Europe, allowing GPs to access the capital required to maintain investment pace and opportunistically target bigger deals. Typically offered with reduced or no management fee and carry, they can also be an effective fundraising sweetener, blending down an LP’s overall costs.

Meanwhile, at a time of economic and geopolitical uncertainty, investors welcome the opportunity to observe the manager in action, and to kick the tyres on specific deals rather than entering a blind pool.

Where Next?

Traditional, closed-end fundraising aimed at institutional investors is not going away, but private markets have continued to generate strong performance. As interest rates ease and deal activity begins to normalise, the wheels will undoubtedly begin turning once again.

However, advances in access to private markets with the retailisation of private funds, the proliferation of SMAs, the globalisation of LP bases and the evolution of the continuation vehicle and co-investment markets over the past three years, all stand managers in good stead as they seek to continue to grow AUM through the cycles.

This article follows a recent podcast with Tom Alabaster, Head of the Private Funds Group in EMEA at Ropes & Gray, and Jeremy Dennison, General Counsel at Livingbridge, hosted by Caplink Group. Tom and Jeremy discuss the expansion of private wealth and how managers are adapting their operations to an increasingly complex market environment. Click here to listen.

This article is the latest in our series of European Private Capital Insights. To subscribe to these and other insights by topic please click here

Authors

Stay Up To Date with Ropes & Gray

Ropes & Gray attorneys provide timely analysis on legal developments, court decisions and changes in legislation and regulations.

Stay in the loop with all things Ropes & Gray, and find out more about our people, culture, initiatives and everything that’s happening.

We regularly notify our clients and contacts of significant legal developments, news, webinars and teleconferences that affect their industries.