We are pleased to announce that Ropes & Gray LLP has formed a dedicated asset management M&A team, co-chaired by Ariel Deckelbaum, Scott Abramowitz and Greg Davis, which includes more than 180 attorneys from various practice areas, including our asset management, M&A, tax and employee benefits practice groups. We look forward to meeting with our clients and friends to discuss how our knowledge and experience in this area may be helpful to you. To mark the launch of this new team, we would like to share some observations on the current state of the market.

To begin, we note that it is hard to talk about asset management deal activity these days without turning to the topic of asset management M&A. Transactions involving the asset managers themselves—whether between one manager and another in a consolidation or growth play or with third parties seeking exposure to GP economics or to assist with generational transitions—have been steadily on the rise for several years. Managers who have traditionally earned healthy fees for deploying third-party capital into operating companies are increasingly considering transactions for the house account. In an M&A environment that has been increasingly challenged of late, these are some of the largest and most high-profile transactions to be announced. Asset management M&A transactions have taken a variety of forms but largely consist of control transactions, minority stakes, lift-outs, lift-ins and joint ventures.

Below, we take a broad look at market trends and key terms.

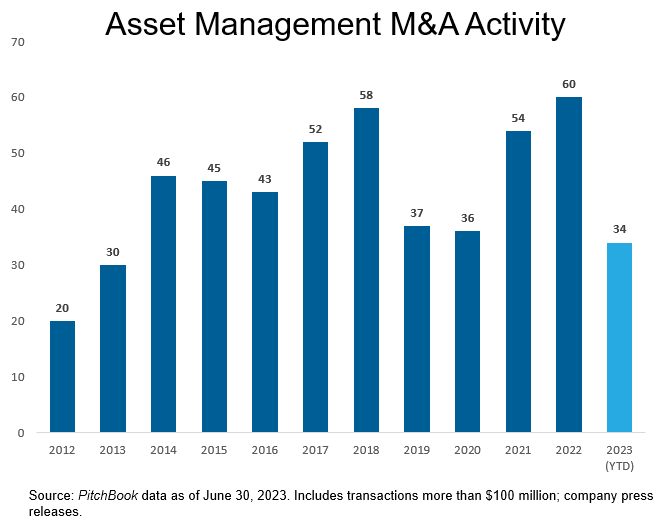

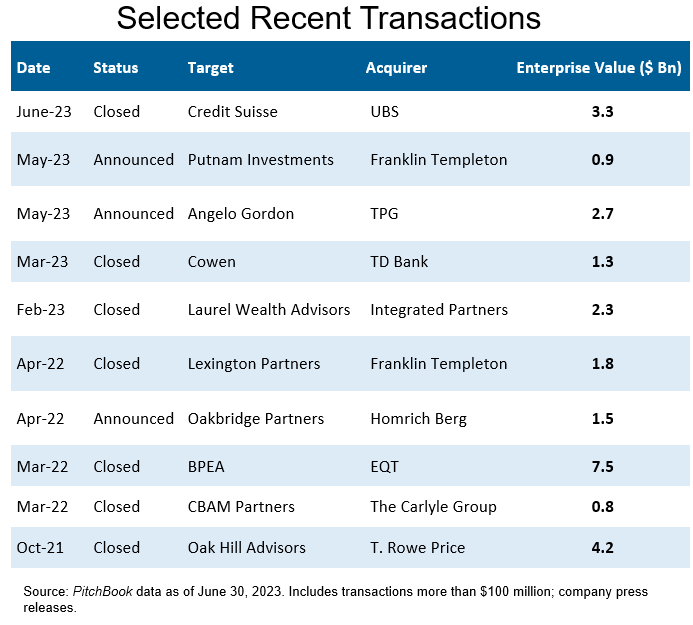

- The Numbers. To begin, here is a snapshot of some recent market data.

Click to Enlarge

Click to Enlarge - Drivers. The old adage that “bigger is better” has taken hold in the asset management industry. Not only have managers raised increasingly larger funds, but they have also sought to grow their firms by acquiring additional AUM in the same or parallel strategies. Similarly, as managers have sought to institutionalize their firms and ensure their staying power, they have tried to build more diversified platforms, adding new and often complementary products that can deliver a broader fee-generating platform and better withstand macroeconomic shifts. Asset management M&A transactions have therefore sought to add AUM, new managers and new platforms, as well as geographic diversity.

- Access to Alternatives. Registered fund sponsors have sought to diversify their retail product offerings by adding on alternatives platforms, while traditional LPs and dedicated funds seek minority stakes and participation in the GP economics of private equity, real estate, and hedge and credit firm managers. As wirehouses and feeder platforms seek to provide retail investors with access to privately offered funds and investments that have historically been available only to institutional investors and ultra-high-net-worth individuals, M&A is a tool being used to accelerate such expansion.

- Market Participants. No one is immune. Recent transactions have seen participation from a wide variety of participants. Of course, it all starts with willing managers—but given the attractive valuations that have been available, the potential liquidity opportunity for founders in parallel with permanent capital to fund growth and participation by future generations, there has been no lack of managers who see a once-in-a-lifetime chance to address succession or grow their platform. At the same time, the number of potential investors has been steadily increasing. Much of this trend started with investors seeking stakes to benefit from GP economics by means of equity investments, revenue-sharing arrangements or structured financings. Insurance managers and pension funds were also early participants because they wanted preferred access to investment opportunities and, in some cases, saw their initial investment as a stepping stone to a control stake through which they could actively manage their assets “in house.” More recently, the demand by retail investors for access to alternatives has led registered fund sponsors to invest in or develop such platforms.

- Key Terms – Economics. With the number of potential investors and pools of capital growing faster than the number of mature managers, it is no surprise that valuations have increased markedly. Even in the current economic environment, which has challenged the valuation of many companies, managers are still able to attract double-digit multiples for their management fees. However, unlike minority stakes, which are largely acquired for cash, most control transactions have been funded by a combination of cash and stock, with the stock component often constituting a majority of the consideration. In addition, many transactions include some form of earnout that is tied to future performance or growth.

- Key Terms – Management. The ability to retain management is the sine qua non of almost every asset management M&A transaction. Management is typically incentivized through a combination of carrots and sticks that include ring-fenced compensation pools and bonus opportunities, vesting and forfeiture of non-cash consideration in the event of early termination (with exceptions for death, disability, good reason and termination without cause) and a suite of restrictive covenants. The typical commitment period is five years, but it can range from three to seven years.

- Key Terms – Governance. Many asset management combinations are similar to joint ventures in that two or more teams come together to build on their respective strengths while needing to protect their individual assets, at least for some initial period (especially in order to retain the team for the initial commitment period as well as the ability to realize any deferred consideration such as an earnout). Outlining the scope of each party’s responsibilities is critical to setting expectations and aligning on the path to success. The topics that arise most often in addressing governance include defining oversight over day-to-day operations, investment decisions, hiring and firing decisions, as well as authority over strategic decisions such as budget, future M&A, the incurrence of debt, liability management, GP economics, and decisions to launch or terminate funds or strategies. Arrangements as to these matters may also lead to discussions about board or committee representation.

- Key Terms – Legal. Like any M&A transaction, it is important for the parties involved to address contingencies and allocate both execution risk and exposure to historical liabilities. Given that asset management transactions are valued based on AUM and the ability to generate recurring fee revenue, it is common to provide for conditions that address minimum AUM and client consents. These are often observed in control transactions in which there may be an adjustment to the purchase price relative to a specified client consent threshold as well as a related condition. Other common adjustments to purchase price often address working capital, indebtedness (including severance, bonus and similar liabilities) and transaction expenses. Transaction agreements also include extensive representations and warranties, though, like in other facets of the M&A marketplace, indemnification is often limited through the use of a representation and warranty insurance policy.

- Key Terms – Tax. When equity consideration is used, it is important to structure the transaction to achieve tax deferral for the equityholders of the target. As with any M&A transaction in which retaining and incentivizing management is paramount, there is often tension between the buyer’s desire to make management’s receipt of consideration contingent on future employment, on the one hand, and sell-side management’s desire to obtain capital gains treatment, on the other. In many cases, this tension can be managed by imposing employment restrictions on stock consideration rather than cash consideration or by using an earnout based on performance metrics rather than employment.

Finally, we note that, unlike in prior cycles, it appears that this subset of the M&A marketplace is here to stay. M&A among managers is now recognized and deployed as a tool to address long term strategies and is part of the regular discourse on planning for the future. We are pleased to share our observations and experience in the hope that they may be helpful to you.

Stay Up To Date with Ropes & Gray

Ropes & Gray attorneys provide timely analysis on legal developments, court decisions and changes in legislation and regulations.

Stay in the loop with all things Ropes & Gray, and find out more about our people, culture, initiatives and everything that’s happening.

We regularly notify our clients and contacts of significant legal developments, news, webinars and teleconferences that affect their industries.