On July 25, 2023, the Departments of the Treasury (Treasury), Labor (DOL), and Health and Human Services (HHS) (collectively, the Departments) proposed rules that would implement amendments made to the Mental Health Parity and Addiction Equity Act (MHPAEA) in 2021. The much-anticipated guidance is intended to provide clarity for group health plans and health insurance issuers for how to comply with new MHPAEA requirements to perform and document comparative analyses of the design and application of non-quantitative treatment limitations (NQTLs)1 in order to assess the impact of an NQTL on access to mental health and substance use disorder benefits as compared to medical or surgical benefits. Additionally, the proposed rules would amend existing NQTL standards to prevent plans and issuers from using them to place greater limits on access to mental health or substance use disorder benefits. The proposed rules, which were issued along with a technical release and the Departments’ second annual report to Congress on compliance with MHPAEA’s comparative analyses requirements, will be subject to a 60-day notice-and-comment period upon publication in the Federal Register.

Given their breadth and complexity, the proposed rules are expected to elicit a significant number of comments from stakeholders. Plans and issuers are advised to start becoming familiar with these rules now—because if finalized as currently contemplated, all provisions (except for those separately implemented by HHS) would apply on the first day of the first plan year beginning on or after January 1, 2025. The provision of the proposed HHS regulations extending MHPAEA requirements to health insurance issuers offering individual health insurance coverage would be effective January 1, 2026, while the provision previously allowing plans to opt out of MHPAEA would be retroactively sunset on December 29, 2022. This Alert provides a high-level overview of the changes the proposed rules would make. We will continue to monitor this rulemaking initiative as it makes its way through the regulatory process.

Background

MHPAEA was signed into law in 2008 to prevent group health plans and health insurance issuers that provide mental health or substance use disorder benefits from imposing less favorable benefit limitations on those benefits than on medical or surgical benefits. The law, as amended, generally requires that plans and issuers offering group or individual health insurance coverage ensure that any financial requirements (such as coinsurance and copays) and treatment limitations (such as visit limits) that apply to mental health and substance use disorder benefits are no more restrictive than the predominant financial requirements or treatment limitations that apply to substantially all medical/surgical benefits in a benefits classification. When MHPAEA was amended by the Consolidated Appropriations Act, 2021, a provision was added that requires plans and issuers to perform and document comparative analyses of the design and application of their NQTLs to demonstrate parity and provide those analyses to the Departments or to an applicable state authority upon request. The MHPAEA amendments also require the Departments to report to Congress annually on the results of these NQTL comparative analysis reviews.

Based on the Departments’ first two reports to Congress since adoption of the comparative analysis requirements, it is clear that compliance remains a major concern. To try and address these deficiencies, enforcement efforts have focused on certain priority areas such as prior authorization requirements for in-network and out-of-network inpatient services; concurrent care review for in network and out-of-network inpatient and outpatient services; standards for provider admission to participate in a network, including reimbursement rates; out-of-network reimbursement rates (e.g., methods for determining usual, customary, and reasonable charges); impermissible exclusions of key treatments for mental health conditions and substance use disorders; and adequacy standards for mental health and substance use disorder provider networks.

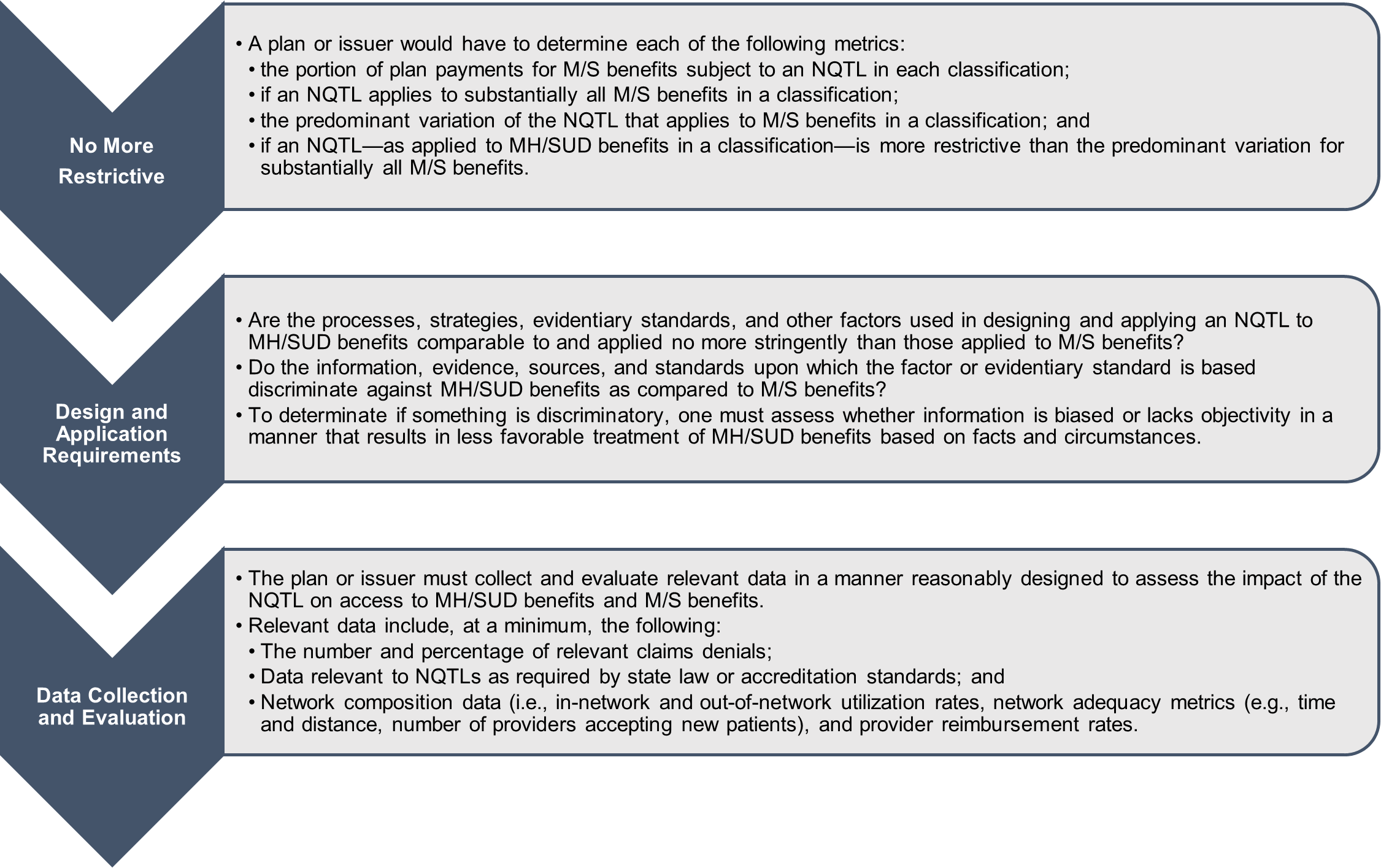

New Conditions for NQTLs to Be MHPAEA-Compliant

As depicted in the diagram below, the proposed rules introduce a new framework for determining whether a plan or issuer has designed and implemented an NQTL that imposes greater limits on access to mental health and substance use disorder benefits as compared to medical/surgical benefits. This framework builds upon the existing MHPAEA regulations that were promulgated in 2013, which established six classifications of benefits: (1) inpatient, in-network; (2) inpatient, out-of-network; (3) outpatient, in-network; (4) outpatient, out-of-network; (5) emergency care; and (6) prescription drugs. Moreover, the 2013 regulations state that if a plan or health insurance coverage provides mental health or substance use disorder benefits in any classification of benefits, the mental health or substance use disorder benefits must be provided in every classification in which medical or surgical benefits are provided.

Abbreviations: MH/SUD = mental health/substance use disorder; M/S = medical/surgical; NQTL = non-quantitative treatment limitations.

The proposed rules provide that if a plan were to fail to satisfy any of the new requirements with respect to an NQTL in a classification, that NQTL would violate MHPAEA and could not be imposed on mental health or substance use disorder benefits in the classification. Furthermore, if a plan or issuer were to fail to satisfy these NQTL requirements, it would have to make changes to the terms of the plan or coverage or the way the NQTL is designed or applied in order to ensure compliance with MHPAEA. According to the proposed rules, plans and issuers would be required to ensure that they are complying with MHPAEA’s requirements at all times when an NQTL is imposed with respect to mental health or substance use disorder benefits, and plans and issuers would be required to confirm that they have performed and documented comparative analyses for the NQTLs imposed on their mental health or substance use disorder benefits to ensure compliance.

Notably, the proposed rule introduces a new requirement for plans to collect and evaluate outcomes data and to measure the impact of NQTLs. This requirement, as described further below, requires plans to evaluate the following: (1) the health plan’s actual provider network, (2) how much it pays out-of-network providers, (3) how often prior authorizations are required, and (4) how often such requests are denied. We expect this to have significant impact on access to care as plans will now be required to carefully examine where they are failing to provide access to mental health care. Importantly, the rule effectively creates a presumption of noncompliance that plans must rebut through careful documentation and evidence to support their coverage decisions.

That said, the proposed rules include a couple of narrow exceptions for when an NQTL that fails to satisfy the new requirements may still be permissible without triggering a violation of MHPAEA. The first exception covers NQTLs that impartially apply generally recognized independent professional medical or clinical standards (consistent with generally accepted standards of care) to medical/surgical benefits and mental health or substance use disorder benefits. The second exception applies to NQTLs that are appropriately designed and carefully circumscribed measures used solely for the purpose of detecting or preventing and proving fraud, waste, and abuse based on indicia of fraud, waste, and abuse that have been reliably established through objective and unbiased data.

- Generally recognized medical/clinical standards – Could apply to NQTLs that fail to satisfy any of the three requirements shown above.

- Fraud or waste – Could apply to NQTLs that fail to meet the no more restrictive requirement, however, the NQTL would still have to comply with the design and application and data evaluation requirements.

New Conditions for NQTLs to Be MHPAEA-Compliant: Network Composition

As indicated above, the data collection requirement includes specific details about network composition, since that is an area of particular interest to the Departments. There is concern that NQTLs related to network composition significantly affect access to mental health and substance use disorder benefits, and as a result, the Departments are of the view that material differences in access based on outcomes data related to NQTLs should be subject to a higher level of scrutiny than for other types of NQTLs. The proposed rules include a special provision for NQTLs related to network composition that says that when designing and applying one or more of these types of limitations, a plan or issuer will be deemed to fail to meet the parity requirements of MHPAEA if, in operation, the relevant data collected show material differences in access to in-network mental health or substance use disorder benefits as compared to in-network medical/surgical benefits in a classification.

In articulating this standard, however, the Departments acknowledge the lack of established and universal metrics for determining the parity of networks2 and the fact that parity across mental health and substance use disorder and medical/surgical networks does not mean there has to be equal numbers of providers in each classification. To help plans and issuers more accurately evaluate any NQTLs they use related to network composition for purposes of conducting their required comparative analyses, the Departments simultaneously issued Technical Release 2023-01P, which outlines four specific types of data that the Departments are considering to require that plans and issuers collect and evaluate as part of their comparative analyses for NQTLs related to network composition. The Departments believe these types of data would generally be relevant for evaluating the impact of all NQTLs related to network composition on access to in-network providers of mental health and substance use disorder services in comparison to in-network providers of medical/surgical services. The four types of data are as follows:

- Out-of-network utilization – This category would encompass the collection of data for medical/surgical as well as mental health and substance use disorder benefits for certain types of items and services such as:

- Inpatient, hospital-based services;

- Inpatient, non-hospital-based services (i.e., inpatient rehabilitation facilities and skilled nursing facilities for medical/surgical items and services and non hospital based inpatient facilities and residential treatment facilities for mental health and substance use disorder items and services);

- Outpatient facility-based items and services (i.e., physical, occupational, speech, and cardiovascular therapy, surgeries, radiology, and pathology; intensive outpatient and partial hospitalization services for mental health conditions or substance use disorder services in an outpatient facility setting);

- Outpatient office visits; and

- Other outpatient items and services.

The Departments are considering requiring plans and issuers to collect and evaluate relevant out-of-network utilization data from the two most recent and complete calendar years that ended at least 90 days prior to the start of the plan or policy year during which the comparative analysis was conducted.

- Percentage of in-network providers actively submitting claims – This category focuses on collecting data regarding the frequency with which different types of in-network mental health or substance disorder providers and medical/surgical providers submitted claims for unique participants, beneficiaries, and enrollees. In particular, the Departments would require including in comparative analyses both the percentage of in-network providers who submitted no in-network claims and the percentage of in-network providers who submitted claims for fewer than five unique participants, beneficiaries, and enrollees during a period.

-

Time and distance standards – According to the Departments, plans and issuers that impose NQTLs related to network composition should be required to collect and evaluate relevant data on the percentage of participants, beneficiaries, and enrollees that would be able to access one or more providers of specified types within a certain time and distance. The proposed rules would require collecting and evaluating data within a specified time and distance by county-type designation regarding access to one (or more) in-network providers within mental health or substance use disorder provider categories (including psychiatry, inpatient care, residential treatment, mobile crisis units, opioid treatment providers, child and adolescent providers, geriatric providers, eating disorder providers, and autism spectrum disorder providers) and one (or more) in-network providers within certain medical/surgical provider categories.

In order to ensure there is sufficient relevant data for plans and issuers to evaluate and consider the impact of this type of network composition NQTL, the Departments are considering requiring plans and issuers to collect and evaluate relevant time and distance data for a specified period of time that ended at least 90 days prior to the date on which a comparative analysis is conducted.

-

Reimbursement rates – The Departments recognize that lower reimbursement rates and higher demand for services from mental health and substance use disorder providers are significant contributing factors to the difficulty that participants, beneficiaries, and enrollees have in finding in-network mental health or substance use disorder providers as compared to in-network medical/surgical providers. Consequently, the Departments have proposed requiring plans and issuers to collect and evaluate relevant data comparing in-network payments and billed charges for mental health or substance use disorder benefits and medical/surgical benefits in the inpatient, in-network and outpatient, and in-network classifications (for office visits and all other benefits), as well as the allowed amounts for specific Current Procedural Terminology (CPT) codes that are reimbursed to specific types of mental health or substance use disorder providers and medical/surgical providers, to compare them to each other as well as to Medicare rates or a similar benchmark.

The Departments are considering requiring plans and issuers to collect and evaluate relevant reimbursement rate data from the two most recent and complete calendar years that ended at least 90 days prior to the start of the plan or policy year during which the comparative analysis was conducted. For example, for a comparative analysis conducted during a plan or policy year beginning January 1, 2026, the plan or issuer would be required to collect and evaluate data from calendar years 2023 and 2024.

Technical Release 2023-01P provides that the Departments would use the four types of data to assist with their respective reviews and evaluations of whether a plan or issuer’s NQTLs related to network composition comply with MHPAEA. Furthermore, the Departments intend to create an enforcement safe harbor with respect to NQTLs related to network composition for plans and issuers that meet or exceed specific data-based standards to be identified in future guidance. Plans and issuers that satisfy the terms of the safe harbor would not be subject to an enforcement action by the Departments under MHPAEA with respect to NQTLs related to network composition for a certain period of time that would be specified in the future guidance.

Contents of an NQTL Comparative Analysis

As mentioned earlier, the 2021 amendments to MHPAEA added a requirement that plans and issuers perform and document comparative analyses of the design and application of their NQTLs to demonstrate parity and provide those analyses to the Departments or to an applicable state authority upon request. The proposed rules set out standards for what a comparative analysis must include to satisfy the statutory requirements of MHPAEA. According to the proposed rules, a comparative analysis must provide, with respect to each NQTL imposed under a plan or coverage option on mental health or substance use disorder benefits, the following six elements at a minimum:

- A description of the NQTL;

- The identification and definition of the factors used to design or apply the NQTL;

- A description of how factors are used in the design or application of the NQTL;

- A demonstration of comparability and stringency, as written;

- A demonstration of comparability and stringency in operation; and

- Findings and conclusions.

Furthermore, each plan or issuer would be required to prepare and make available to the Departments or applicable State authorities, upon request, a written list of all NQTLs imposed under the plan or coverage and a general description of any information considered or relied upon by the plan or issuer in preparing the comparative analysis for each NQTL. Also, for plans subject to ERISA, the proposed rules would require that the plan or issuer provide this list and a general description to the named fiduciaries required to review the findings or conclusions of each comparative analysis.

Enforcement Authority under ERISA

The Departments acknowledge in the proposed rules that in practice, plan sponsors often rely on the issuer of fully insured plans, third-party administrators (TPAs) of self-insured plans, and other service providers to administer their benefits, including designing and implementing the limitations and coverage terms that are subject to MHPAEA requirements and providing them with comparative analyses (or the necessary information for the sponsors to produce their own comparative analyses) for the NQTLs that the issuers, TPAs, and service providers design and apply to mental health and substance use disorder benefits and medical/surgical benefits under the terms of the plan or coverage. Moreover, while the states and HHS have enforcement authority over issuers providing health insurance coverage with respect to fully insured plans, the Departments have limited direct enforcement authority over other service providers (such as the TPA of a self-insured health plan). Nonetheless, the proposed rules note how under ERISA, such service providers may be fiduciaries with respect to private employment-based group health plans. To the extent that such service providers are fiduciaries for such plans—something we expect they will go to great lengths to avoid—they remain subject to ERISA’s provisions governing fiduciary conduct and liability, including the provisions for co-fiduciary liability under ERISA Section 405. As a result, the Departments state that they will use all available authority to ensure compliance by plans and issuers with MHPAEA for all entities that play a role in administering and designing benefits.

HHS Proposed Regulations

In addition to the changes proposed by the Departments that are described above, HHS also proposes the following regulatory amendments:

- Applicability to individual health insurance coverage – Currently, MHPAEA applies to health care coverage offered by a health insurance issuer in connection with a group health plan in a large-group market. The proposed rule would extend MHPAEA requirements to health insurance issuers offering individual health insurance coverage for policy years beginning on or after January 1, 2026.

- Sunset of the MHPAEA opt-out provision – The proposed rule would implement the sunset provision for self-funded, non-federal governmental plan elections to opt out of compliance with MHPAEA, as enacted in the Consolidated Appropriations Act, 2023. Specifically, the sponsor of a self funded, non-federal governmental plan may not elect to exempt its plans from any of the MHPAEA requirements on or after December 29, 2022. Further, any opt-out election that expires on or after June 27, 2023 cannot be renewed. As a result, these plans must comply with MHPAEA unless a separate exemption applies.

If you have any questions, please reach out to your usual Ropes & Gray advisor.

- NQTLs are generally plan provisions that impose non-numerical limits on the scope or duration of benefits. Expanding on the existing MHPAEA regulations that were adopted in 2013, the proposed rules include an updated, illustrative list of NQTLs that includes but is not limited to the following:

- Medical management standards (such as prior authorization) limiting or excluding benefits based on medical necessity or medical appropriateness or based on whether the treatment is experimental or investigative;

- Formulary design for prescription drugs;

- For plans with multiple network tiers (such as preferred providers and participating providers), network tier design;

- Standards related to network composition, including, but not limited to, standards for provider and facility admission to participate in a network or for continued network participation, including methods for determining reimbursement rates, credentialing standards, and procedures for ensuring the network includes an adequate number of each category of provider and facility to provide services under the plan;

- Plan methods for determining out-of-network rates, such as allowed amounts; usual, customary, and reasonable charges; or application of other external benchmarks for out-of-network rates;

- Refusal to pay for higher-cost therapies until it can be shown that a lower-cost therapy is not effective (also known as fail-first policies or step therapy protocols);

- Exclusions based on failure to complete a course of treatment; and

- Restrictions based on geographic location, facility type, provider specialty, and other criteria that limit the scope or duration of benefits for services provided under the plan.

- For instance, while many plans and issuers rely on minimum time and distance standards set by private accreditation organizations or by other federal or state programs, the Departments state that this cannot be the sole basis or evidentiary standard upon which to design and apply an NQTL.

Stay Up To Date with Ropes & Gray

Ropes & Gray attorneys provide timely analysis on legal developments, court decisions and changes in legislation and regulations.

Stay in the loop with all things Ropes & Gray, and find out more about our people, culture, initiatives and everything that’s happening.

We regularly notify our clients and contacts of significant legal developments, news, webinars and teleconferences that affect their industries.